This is one of those few times during the Earth’s solar year that one can look around and know exactly where on the calendar they are. I’m speaking from my vantage point of the United States, of course, as it’s the only Earth community I’ve visited since I took up residence some seven years ago. Nevertheless, I’m betting the same can be said for most places on the planet at this time of year.

I’m referring to the month of December and the holiday season. The most brilliant indicators are the lights and decorations – once again, I’ve opted to partake in the festivities and have installed some additional exterior illumination on my spaceship in the form of icicle lights and a blow mold snow family. Next year, I’m thinking about incorporating a massive 25-foot inflatable Grinch to my display – not because I’m a Grinch (I’m very far from it!) but because he reminds me of an uncle of mine back on Amicitia.

I’m referring to the month of December and the holiday season. The most brilliant indicators are the lights and decorations – once again, I’ve opted to partake in the festivities and have installed some additional exterior illumination on my spaceship in the form of icicle lights and a blow mold snow family. Next year, I’m thinking about incorporating a massive 25-foot inflatable Grinch to my display – not because I’m a Grinch (I’m very far from it!) but because he reminds me of an uncle of mine back on Amicitia.

In the credit union mortgage lending universe, it’s the time of year when we can assist our members in attaining the biggest gift of the season: a new home! Oftentimes, the loan originator and/or Realtor involved in making this dream gift a reality congratulates the member in their own way, especially during this time of year. I’ve seen members presented with gift cards to home improvement stores and food delivery services; I’ve seen gadgets that can be used around the new home, like “smart” thermostats; I’ve even seen a door knocker gifted to a new homeowner – for me, that’s a bit too reminiscent of Scrooge’s haunted knocker in A Christmas Carol!

Myself, I think a more personalized gift is the way to go, and I wanted to share an idea around one such option. Find a recipe that you simply love or that has some significance to you or your family. Present it to your member with either the actual “dish” that you prepared for them or a basket containing all the ingredients needed to prepare it themselves. There are a lot of ways to further customize and personalize this gift, so be creative! (And keep reading to the end of this post for a special gift I have for you!)

As we talk about gifts during the homebuying process, I’d be remiss if I didn’t mention what typically comes to mind when a mortgage professional hears the word “gift.” That would be the gifting of funds to a borrower to assist with down payment or closing costs. There are other ways these funds can be used, but down payments and closing costs are by far the most common application of these gifted funds.

When a member is buying a home, we all know of the various costs that can be associated with it, so having all the funds needed to close the loan while still ensuring money is available for ongoing costs and emergencies can be a stretch. That’s why in many cases, gifted funds are a perfectly acceptable solution… but only if they are gifted and presented correctly.

It’s important for us – your member’s trusted mortgage partners – to ensure that key requirements of gift funds are met. Work closely with your members to inform and educate them on what is required, including:

- Acceptable Donors: Funds can generally be gifted by family members; depending on the specific type of loan (e.g., FHA, Conventional), other resources could include friends, employers, unions and charities. Be sure your member knows exactly who can assist them.

- Gift Letters: A signed document from the donor must be received, stating that the funds are a gift and NOT a loan. It should include the borrower’s name, their relationship, the amount of the gift and the date.

- Bank Statements: The donor needs to provide these to show the money originated from them and wasn’t borrowed.

- Proof of Funds Transfer: Evidence showing the money was moved from the donor’s account to the borrower or directly to the title company must be provided – the previously mentioned bank statements could potentially provide this information.

- Donor Contribution Tax Rules: Be sure to communicate that donors should consult with their tax professional to determine if their gift is subject to being taxed or is exempt.

- Other Important Considerations: Depending on the loan type, inform your member of specifics around gifted funds associated with their mortgage. For example, gift funds can often cover the entire down payment for FHA loans while for some conventional loans, the borrower may still need to have some “skin in the game” with their own funds.

It’s important to be well-versed in the dos and don’ts of gifted mortgage funds. It’s a great way to ensure your member’s loan is viable, but it must be done right! It’s like following a recipe – make sure you have all the necessary ingredients and follow each step to create something special!

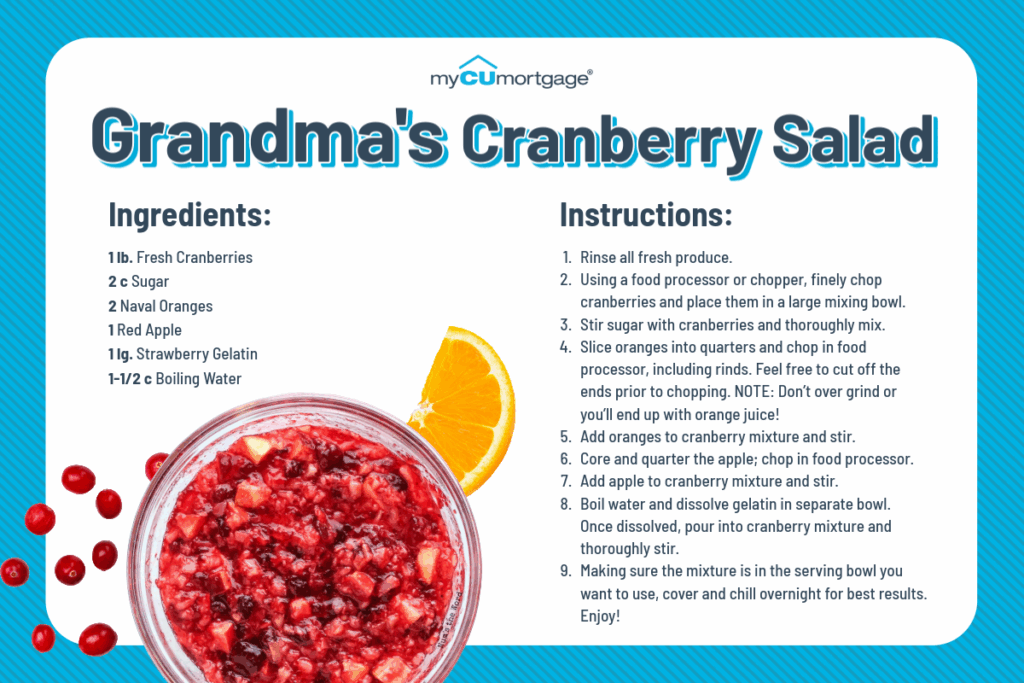

Speaking of recipes, I promised I had a holiday gift for all of you. As part of many holiday traditions, the cranberry has inserted itself as a staple in many dishes (and even decorations). Personally, I have never been a fan – they are too bitter for my liking. However, a colleague told me he made a cranberry salad that would change my mind. Not only did it change my thoughts on cranberries, but the taste blew my mind! So, I’d like to share this sensational taste experience with you.

I convinced my colleague to share his secret recipe, which you can Download Here. In full transparency, he accredited it to his grandma who used to create this treasure every year during the holidays. Seeing as there were no automated food processors back in her day, this becomes an even more impressive accomplishment!

Enjoy Grandma’s Cranberry Salad as you enjoy the rest of the holiday season. And consider it for your get-togethers during the upcoming Christmas holiday, the current festival of Hanukkah and all other seasonal celebrations. It’s a great gift for all those who partake!